Model Beneisha (M-score) – 1999

Method of calculation

where:

Model description

The probit Beneish Model (M-score) is one of the most well-known method of detecting earnings manipulation.

Prof. M. D. Beneish from the Indiana University analyzed financial data of Amercian listed companies for 1982-1992. The sample included also firms that manipulate earnings.

The model uses three groups of ratios (variables):

- ratios illustrating the future performance of a company,

- ratios related to cash flows and accruals,

- ratios indicating the motivation of managers to manipulate financial data.

The original model includes eight variables (ratios). The variables are measured using data from the fiscal year of the first reporting violation (t) by comparing them to the prior year (t - 1). For each variable the coefficient was estimated.

Interpretation of the M-score

- M > -2.22 (-1.78) – the value above threshold indicates that there is likelihood of earnings manipulation. The value -1.78 results from the correction introduced in 2012.

- The model identifies correctly potential manipulators for:

- 76% cases in the first year after the earnings manipulation,

- 66% cases in the second year after the earnigns manipulation.

- Based on the analysis of the firms that manipulated earnings, Beneish noticed, that on average, manipulators have significantly:

- higher growth of sales,

- larger accruals,

- greater deterioration of gross margins and assets quality,

- larger increase in debt,

- larger increases in days sales in receivables.

- Notes on the interpretation and application of the model:

- the model assesses the likelihood of earnings manipulation and enables to classify firms as "manipulators" or "non-manipulators",

- for the model to be effective the company in period (t - 1) cannot manipulate the earnings, otherwise comparing data from two manipulated periods will give incorrect results

- individual ratios are only a signal of a potential manipulation, which may indicate further directions of detailed analysis (e.g. cost level analysis, analysis of the cause of changes in the level of sales and receivables),

- it should be checked whether there were any changes in the assumptions of the company's accounting policy in the analyzed period.

Detailed description of respective ratios and their impact on the M-score value

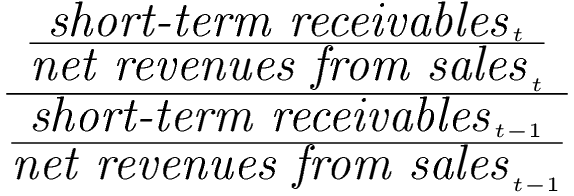

DSRI – days sales in receivables index

Method of calculation

Ratio's weight: +0.920

Units: times

Value for "manipulators": 1.412

Value for "non-manipulators": 1.030

Remarks

The value for the first period (first column in the table) is equal to the value for the current period (t), as the value for the previous period (t-1) is not available.

Ratio's interpretation

- DSRI is the ratio of days sales in receivable in the first year in which earnings manipulation is uncovered (year t) to the corresponding measure in year t - 1. This variable gauges whether receivables and revenues are in or out-of-balance in two consecutive years.

- Disproportionate increases in receivables relative to sales may be suggestive of revenue inflation.

- It is expected that a large increase in days sales in receivables is associated with a higher likelihood that revenues and earnings are overstated.

- However a large increase in days sales in receivables could be the result of a change in credit policy (it should be checked).

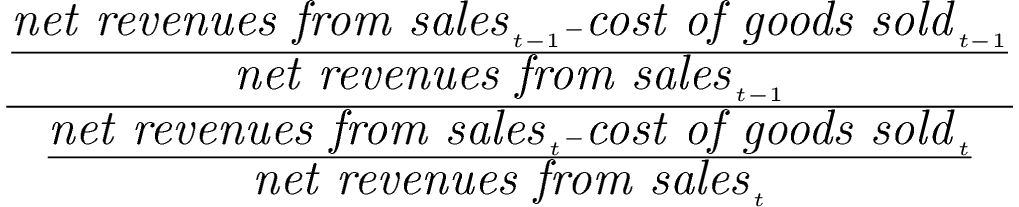

GMI – gross margin index

Method of calculation

Ratio's weight: +0.528

Units: times

Value for "manipulators": 1.159

Value for "non-manipulators": 1.017

Remarks

The value for the first period (first column in the table) is equal to the value for the current period (t), as the value for the previous period (t-1) is not available.

Ratio's interpretation

- GMI is ratio of the gross margin in year t - 1 to the gross margin in year t.

- When GMI is greater than 1, it indicates that gross margins have deteriorated.

- Firms with poorer prospects are more likely to engage in earnings manipulation, thus it is expected to be a positive relation between GMI and the probability of earnings manipulation.

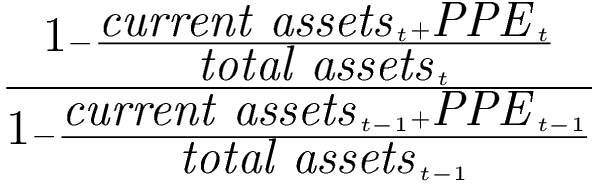

AQI – asset quality index

Method of calculation

Ratio's weight: +0.404

Units: times

Value for "manipulators": 1.228

Value for "non-manipulators": 1.031

Remarks

The value for the first period (first column in the table) is equal to the value for the current period (t), as the value for the previous period (t-1) is not available.

Ratio's interpretation

- AQI is the ratio of asset quality in year t, relative to asset quality in year t - 1.

- Asset quality in a given year is the ratio of non-current assets other than property plant and equipment (PPE) to total assets. It measures the proportion of total assets for which future benefits are potentially less certain.

- If AQI is greater than 1 it indicates that the firm has potentially increased its involvement in cost deferral, thus it is expected to be a positive relation between AQI and the probability of earnings manipulation.

SGI – sales growth index

Method of calculation

Ratio's weight: +0.892

Units: times

Value for "manipulators": 1.581

Value for "non-manipulators": 1.133

Remarks

The value for the first period (first column in the table) is equal to the value for the current period (t), as the value for the previous period (t-1) is not available.

Ratio's interpretation

- SGI is the ratio of sales in year t to sales in year t - 1.

- It is expected to be a positive relation between SGI and the probability of earnings manipulation.

- For SGI greater than 1, the likelihood of earnings manipulation is higher.

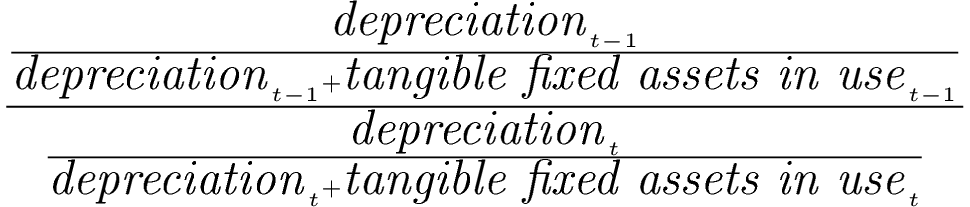

DEPI – depreciation index

Method of calculation

Ratio's weight: +0.115

Units: times

Value for "manipulators": 1.072

Value for "non-manipulators": 1.007

Remarks

The value for the first period (first column in the table) is equal to the value for the current period (t), as the value for the previous period (t-1) is not available.a

Ratio's interpretation

- DEPI is the ratio of the rate of depreciation in year t - 1 versus the corresponding rate in year t.

- A DEPI greater than 1 indicates that the rate at which assets are depreciated has slowed down - decreasing operating costs and increasing net profit.

- It is expected to be a positive relation between DEPI and the probability of manipulation.

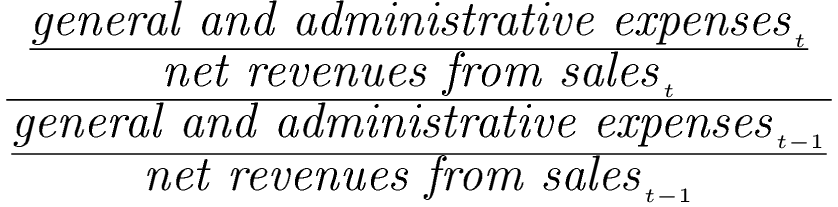

SGAI – sales general and administrative expenses index

Method of calculation

or

Ratio's weight: -0.172

Units: times

Value for "manipulators": 1.107

Value for "non-manipulators": 1.085

Remarks

The first formula applies to the calculation version of PaLS. In the comparative version, since the numerator elements are not available, we assume the second formula.

The value for the first period (first column in the table) is equal to the value for the current period (t), as the value for the previous period (t-1) is not available.

Ratio's interpretation

- SGAI is calculated as the ratio of SGA to sales in year t relative to the corresponding measure in year t - 1.

- A disproportionate increase in SGA is regarded as a negative signal about firms future prospects.

- It is expected to be a positive relation between SGAI and the probability of manipulation.

- SGAI greater than 1 increases the likelihood of manipulation.

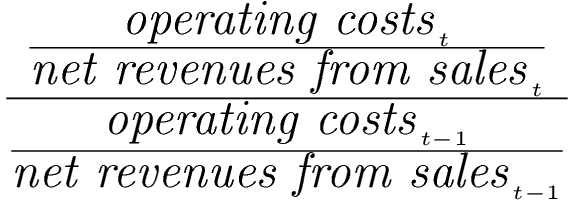

TATA – total accruals to total assets

Method of calculation

or

Ratio's weight: +4.679

Units: times

Value for "manipulators": 0.049

Value for "non-manipulators": 0.015

Remarks

The value for the first period (first column in the table) is equal to the value for the current period (t), as the value for the previous period (t-1) is not available.

Ratio's interpretation

- Total accruals are calculated as the change in working capital accounts other than cash less depreciation.

- Total accruals to total assets is used to proxy for the extent to which cash underlies reported earnings.

- It is expected that higher positive accruals (less cash) are associated with a higher likelihood of earnings manipulation.

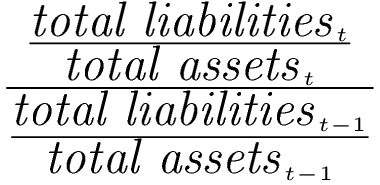

LVGI – leverage index

Method of calculation

Ratio's weight: -0.327

Units: times

Value for "manipulators": 1.124

Value for "non-manipulators": 1.033

Remarks

The value for the first period (first column in the table) is equal to the value for the current period (t), as the value for the previous period (t-1) is not available.

Ratio's interpretation

- LVGI is the ratio of total debt to total assets in year t relative to the corresponding ratio in year t - 1.

- LVGI captures debt covenants incentives for earnings manipulation.

- LVGI greater than 1 indicates an increase in leverage and higher likelihood of manipulation.

Based on:

BENEISH M.D. (1999), The Detection of Earnings Manipulation, "Financial Analysts Journal", vol. 55, no. 5.

BENEISH M.D., LEE C.M.C., NICHOLS C. (2012), Fraud Detection and Expected Returns, Working Paper, Indiana University Bloomington.

DALECKA A. (2015) Użyteczność modelu Beneisha w detekcji manipulacji księgowych, "Finanse, Rynki finansowe, Ubezpieczenia" nr 73, t. 1. (in Polish)